-

CAR INSURANCE

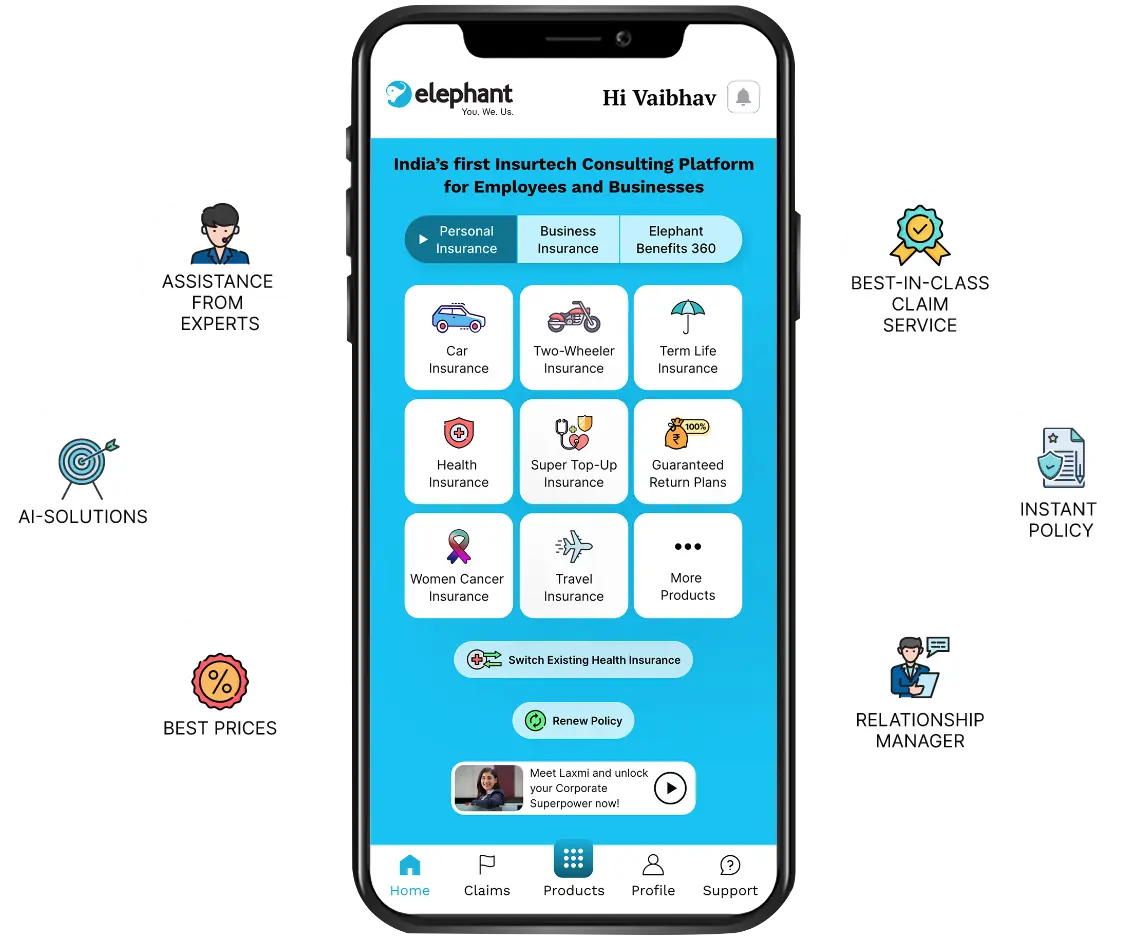

Car InsuranceFlat 80%* OFFGet right cover at best price on your car insurance policy. Unlock your corporate superpower today.GET QUOTESWhat does your car insurance cover you for?Comprehensive coverageLiability coveragePersonal accident coverageZero-depreciation coverMany more add-on coversGet your car insured with the best features - completely online, right now!CloseWhat do you get at Elephant Insurance?Corporate Superpower of best Car Insurance DealsAI-Based Car Insurance RecommendationsHandpicked Insurers for Car InsuranceUnmatched Prices on Car Insurance PremiumsInstant Policy Issuance for your vehicle100% Assistance from ExpertsDigital Relationship ManagerBest-in-Class Claims ServiceLifetime Personalised AccountRenewal Management

-

TWO-WHEELER INSURANCE

Two-Wheeler InsuranceStarting at Rs.546* only.Get right cover at best price and insure your two-wheeler for a joy ride. Unlock your corporate superpower today.GET QUOTESWhat does your two-wheeler insurance cover you for?Comprehensive coverageLiability coveragePersonal accident coverageZero-depreciation coverMany more add-on coversGet your two-wheeler insured with the best features - completely online, right now!CloseWhat do you get at Elephant Insurance?Corporate Superpower of best Two-wheeler Insurance DealsAI-Based Two-wheeler Insurance RecommendationsHandpicked Insurers for Two-wheeler InsuranceUnmatched Prices on Two-wheeler Insurance PremiumsInstant Policy Issuance for your vehicle100% Assistance from ExpertsDigital Relationship ManagerBest-in-Class Claims ServiceLifetime Personalised AccountRenewal Management

-

TERM LIFE INSURANCE

Term Life InsuranceRs.1 crore life cover at Rs.503/month* only.Securing your loved ones future is not expensive, it is priceless! Be a superhero by unlocking your corporate superpower today.GET QUOTESWhat does your term life insurance cover you for?Death benefitsCritical illnesses coverAccidental death benefitWaiver of premiumMany more add-on coversGet your term life insurance with the best features - completely online, right now!CloseWhat do you get at Elephant Insurance?Corporate Superpower of best Term Life Insurance DealsAI-Based Term Life Insurance RecommendationsHandpicked Insurers for Term Life InsuranceHandpicked Insurers for Term Life InsuranceInstant Policy Issuance for you and your family100% Assistance from ExpertsDigital Relationship ManagerBest-in-Class Claims ServiceLifetime Personalised AccountRenewal Management

-

HEALTH INSURANCE

Health InsuranceGet Rs.5 lakh health cover at Rs.18/day* only.Protecting your health is always our priority. Be a superhero by unlocking your corporate superpower today.GET QUOTESWhat does your health insurance cover you for?Unexpected medical billsPre and post hospitalisation billsDay care treatmentsMaternity, newborn care and organ donor expensesMany more add-on coversGet your health insurance with the best features - completely online, right now!CloseWhat do you get at Elephant Insurance?Corporate Superpower of best Health Insurance DealsAI-Based Health Insurance RecommendationsHandpicked Insurers for Health InsuranceUnmatched Prices on Health Insurance PremiumsInstant Policy Issuance for you and your family100% Assistance from ExpertsDigital Relationship ManagerBest-in-Class Claims ServiceLifetime Personalised AccountRenewal Management

-

CYBER PROTECT

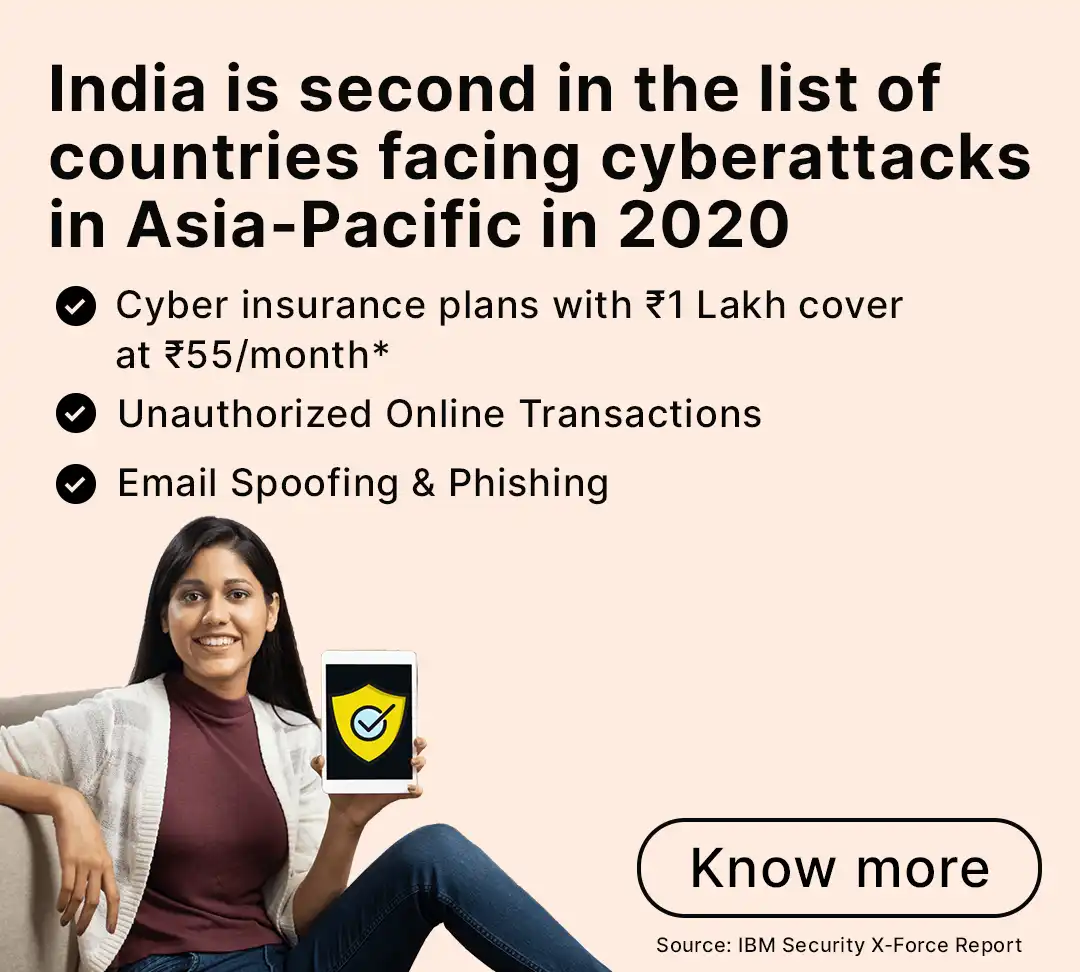

Cyber Protect InsuranceGet Rs.1 lakh cyber protection cover at Rs.55/day* only.Don't be a victim of cyber fraud! Get right cover at best price on your cyber insurance policy. Unlock your corporate superpower today.GET QUOTESWhat does your cyber insurance cover you for?Legal protectionUnauthorised online transaction coverPhishing and email spoofing coverCyber stalking and identity theft coverCyber extortion and many more coveragesGet your cyber insurance with the best features - completely online, right now!CloseWhat do you get at Elephant Insurance?Corporate Superpower of best Cyber Insurance DealsAI-Based Cyber Insurance RecommendationsHandpicked Insurers for Cyber InsuranceUnmatched Prices on Cyber Insurance PremiumsInstant Policy Issuance for your cyber protection100% Assistance from ExpertsDigital Relationship ManagerBest-in-Class Claims ServiceLifetime Personalised AccountRenewal Management

-

OTHER PRODUCTS

Critical Illness InsuranceA must-have protection to secure you against critical illnesses.GET QUOTESPersonal Accident InsuranceAccidents are sudden and can cause damage to your financial planning as well.GET QUOTESClose

Car

Insurance

Insurance

Two-Wheeler

Insurance

Insurance

Term Life

Insurance

Insurance

Guaranteed

Return Plans

Return Plans

Travel

Insurance

Insurance

Cyber

Insurance

Insurance

Health

Insurance

Insurance

Super Top-Up

Insurance

Insurance

Insurance

Women Cancer

Insurance

Insurance

Critical Illness

Insurance

Insurance

Home

Insurance

Insurance

More

Products

Products

Car

Insurance

Insurance

Two-Wheeler

Insurance

Insurance

Term Life

Insurance

Insurance

Guaranteed

Return Plans

Return Plans

Travel

Insurance

Insurance

Health

Insurance

Insurance

Super Top-Up

Insurance

Insurance

Women Cancer

Insurance

Insurance

Insurance

Critical Illness

Insurance

Insurance

Home

Insurance

Insurance

Cyber

Insurance

Insurance

Switch Existing Health Insurance

Switch Existing Health Insurance  Renew Policy

Renew Policy

Products

Products

Powered by Alliance Insurance Brokers Pvt Ltd

Why Elephant Insurance?

We are India's first Insurtech consulting and advisory platform providing a

one-stop solution for all insurance requirements of Corporate Employees.

We were born to empower corporate employees and give them the Muscle of Corporate - Corporate Superpower! And we are not alone in this.

We are backed by India's leading insurance brokering house - Alliance Insurance Brokers Pvt. Ltd., and the legacy continues!

We were born to empower corporate employees and give them the Muscle of Corporate - Corporate Superpower! And we are not alone in this.

We are backed by India's leading insurance brokering house - Alliance Insurance Brokers Pvt. Ltd., and the legacy continues!

Corporate Superpower

Being a corporate employee you have superpowers. With Elephant Insurance,

you can use them to get killer prices and best-in-class service.

AI-based Recommendation

Say hi to Laxmi - the Artificial Intelligence, who is a friendly advisor

and will hand-hold you through the entire process and recommend a solution that is a perfect fit

for you.

Handpicked Insurers

Insurance companies have been handpicked basis their service, prices and

claims paying capability to create a smooth experience.

Right Insurance at Best Price

Being a corporate employee can be advantageous. We ensure you don't get the cheapest insurance but a right insurance

meeting all your needs at the best negotiated price.

Instant Policy

No more waiting for the physical policies, which used to be lengthy and time consuming. Employees can now print or

download the policy immediately after a successful payment!

Assistance from Experts

Getting into the world of insurance can be complicated, but with the

presence of Elephant Insurance, no more! We have leading insurance experts that can help guide

you through the entire process, making it a cakewalk!

Digital Relationship Manager

You may need help any time after you buy a policy and for the same reason,

you get assigned with a dedicated digital relationship manager for any support. Someone's always

there to rescue!

Best-In-Class Claim Service

Things do go wrong! But our experienced and dedicated claims experts will

help you manage your claims effortlessly.

Lifetime Personalized Account

Who doesn't like to have everything under one roof? You will be provided

with a lifetime personalized account for seamless policy management.

Renewal Management

You will get regular automatic renewal notification and reminders before

policy expiry, ensuring the policy is renewed on-time, easily and quickly!

Our exclusive offers. Just for you.

A cost-free employee-benefit initiative for the corporate employees.

30+

Insurers

Insurers

On-boarded with the likes of ICICI Lombard, Bajaj Allianz, HDFC Ergo, Star Health, Tata AIG, Future Generali, Care

(Religare), Go Digit, Max Bupa, HDFC Life, ICICI Prudential, Max Life, Bajaj Allianz Life, Kotak Mahindra, Tata AIA, PNB

Met Life and many more.

500+

Corporates

Corporates

On-boarded with the likes of Vantage Circle, BenefitHub, Trrain Circle, Hexaware, AGS Transact, Wildcraft, Udaan,

Informatica, Jubilant Generics, Wissen, Katerra, IDBI Bank, Privi Organics, Prolifics, Netcore Solutions, Sentiss

Pharma, Edureka and many more.

10+ Lakh

Employees

Employees

Enjoying their Corporate Superpower with Elephant Insurance.

Your one stop insurtech platform now at your fingertips!

Get the Right Insurance at the Best Price, every time with the Elephant.in App. Avail Exclusive Discounts and Corporate Offers on your insurance needs, using your work email id

Download our app from

We make insurance simpler and easier for the corporate employees, by filling the gap in the current insurance market.

The Direct Benefit to the Employers:

It is very common for the employees to feel stressed about the finances, and in such a scenario it directly affects the

businesses and its growth. Financial wellness of the employees is directly related to the overall wellbeing of the

business as if they are financially sound, they will show better productivity towards their work.

It all boils down to choosing the right insurance for your employees, and you can act as the guiding star for them.

Here are a few direct benefits employers can get:

Increase Financial Quotient

It helps employees get more educated and aware about their finances

Structured Planning

It will help employees plan their finances better and be at ease.

Secured Employer Platform

Making insurance management easy for employees, so that they can be more focused and productive at work.

Our latest Insurance articles & videos

-

Published on: 21st Jan 2025How to buy health insurance in Hyderabad: A Comprehensive GuideREAD MORE

Published on: 21st Jan 2025How to buy health insurance in Hyderabad: A Comprehensive GuideREAD MOREThere is a rapid growth in the healthcare sector of the bustling metropolis of Hyderabad which houses a rich culture and IT hub. To protect yourself and your family members from the financial challenges that may occur due to unforeseen medical costs, it is essential that you acquire a health insurance.

In order to provide valuable insights into the different types of health insurance policies available to you, factors and steps you may need to consider and to help you understand the process of acquiring a policy, this guide will assist you throughout.

In India, health insurance serves as a financial cushion, providing coverage for various hospitalization-related medical costs. Having a financial safety net in case of sickness or injury gives you peace of mind.

Benefits of Having Health Insurance in Hyderabad

-

Financial Protection:

-

Cashless Hospitalization:

-

Tax Benefits:

To ensure that you don’t deplete your financial savings due to unforeseen medical costs, health insurance comes into play.

Access to Quality Healthcare:

Quality hospitals and health specialists can be acquired as health insurance opens up multiple such options.

The need for upfront payments is eliminated as many health insurance plans offer cashless hospitalization facilities.

There are numerous tax benefits that one can get for health insurance premiums under Section 80D of the Income Tax Act.

Also Read: Understanding Tax Benefits: How Health Insurance Impacts Your Taxes

Types of Health Insurance Plans in Hyderabad

-

Several types of health insurance plans are available in Hyderabad:

-

Individual Health Insurance:

-

Family Floater Health Insurance:

-

Senior Citizen Health Insurance:

-

Critical Illness Insurance:

A single individual is covered under this plan.

Under a single policy, multiple members of the family are covered.

A policy that caters especially to elderly people.

Upon diagnosis of critical illness, a lumpsum amount is paid to the individual.

Factors to Consider When Buying Health Insurance in Hyderabad

-

Sum Insured:

-

Network Hospitals:

-

Pre-existing Conditions:

-

Add-on Covers:

-

Premium Cost:

-

Claim Settlement Ratio:

Based on your age, health history, and the size of your family, choose an insured sum that perfectly covers the medical costs.

For convenient access to cashless treatments, opt for a plan that covers a wider range of network hospitals in Hyderabad.

Check if the policy you are acquiring covers pre-existing conditions and check if there’s a waiting period.

Take into consideration additional optional health insurance riders like maternity benefits, personal accident cover, or dental coverage.

In order to find the best deal, compare premiums from different insurers.

To understand the efficiency of the health insurance policy thoroughly research the insurance company’s claim settlement ratio.

Also Read: Things to consider while buying health insurance plans

Steps to Buy Health Insurance in Hyderabad

-

Assess Your Needs:

-

Compare Plans:

-

Choose a Plan:

-

Submit Documents:

-

Pay Premium:

Based on factors like your age, health, and size of the family, determine your coverage requirements.

Compare premiums, features, and network of hospitals after obtaining multiple quotes from different insurance companies.

Choose a plan that best aligns with your needs and budget.

Important documents like age proof, income proof, and medical records should be furnished and provided to the insurance company (if applicable).

To activate your insurance policy, make the initial premium payment.

Tips for Managing Your Health Insurance

- Renew your policy in a timely manner.

- Update your insurer about any changes.

- Read your policy and understand the terms and conditions thoroughly.

- Take advantage of all the benefits offered to you under the health policy

- Utilise online services for easy policy management and claims submission.

Conclusion

Buying health insurance in Hyderabad is necessary to protect your financial health. Understanding the various kinds of plans, considerations, and steps can help you choose a policy that suits your specific needs and make an informed decision. Keep in mind, that purchasing a health insurance policy is a way to invest in your well-being and mental stability.

Do you want to know about the health insurance options available to you? Reach out to us by calling 1800 266 9693 via phone or email us at support@elephant.in for further information, or browse Elephant.in website!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/22

-

-

Published on: 18th Jan 2025A Comprehensive Guide to Cashless Medical Insurance in IndiaREAD MORE

Published on: 18th Jan 2025A Comprehensive Guide to Cashless Medical Insurance in IndiaREAD MOREIn today’s increasingly rapid society, having health insurance is crucial because unforeseen medical crisis can occur, putting families at risk financially. Cashless health insurance, a widely favored and convenient choice, provides a security blanket by paying for medical costs without the need for initial payments. Policyholders have the option to get treatment at network hospitals, where the insurance provider will directly pay the bill, instead of paying upfront and waiting for reimbursement later, making the process easier and less stressful.

This guide will provide a comprehensive explanation of cashless medical insurance for individuals who are not familiar with health insurance, covering its definition, advantages, functioning, and important takeaways. Having this information allows you to make educated choices and guarantee that you and your loved ones are financially secure in the event of medical emergencies.

What is Cashless Medical Insurance?

Cashless health insurance policy is a kind of medical insurance that allows policyholders to get treatment without making immediate payments. Instead of paying hospital bills upfront and seeking reimbursement after, the insurance company pays the hospital bill directly. Healthcare providers partnered with the insurance company offer this service at in-network hospitals.

In a place such as India, where healthcare costs can be burdensome, cashless health insurance offers significant relief. In times of crisis, it guarantees access to vital medical treatment without the burden of raising money.

How Cashless Medical Insurance Works

-

Network Hospital Selection:

Treatment under cashless medical insurance is applicable only at in-network hospitals, part of the insurance company’s approved list. Every insurance provider offers a list of network hospitals where the cashless facility can be availed.

-

Hospitalization Process:

For planned hospitalization, advance notice (usually 48-72 hours prior to admission) needs to be provided to the insurance company. In the case of emergency hospitalization, this can be done within 24 hours. Once a network hospital is selected, a pre-authorization form, completed with the assistance of the hospital’s insurance desk, will be submitted to the insurance company for approval.

-

Approval by the Insurance Provider:

After receiving the pre-authorization form, the insurance company verifies that the treatment is covered under the policy. Upon approval, the bill settlement between the hospital and the insurance company takes place directly. The amount covered depends on the sum insured and the policy terms.

-

Final Settlement and Discharge:

After treatment, the hospital sends the final invoice to the insurance provider for settlement. Any costs not covered by the policy, such as consumables or registration fees, must be paid separately. Once the settlement is complete, the patient is discharged without having to pay large bills upfront.

Also Read: Things to know about cashless health insurance

Benefits of Cashless Medical Insurance

-

No Upfront Payments:

One of the biggest advantages is the elimination of the need to arrange funds during medical emergencies, as the expenses are settled directly between the insurance provider and the hospital.

-

Convenience:

Cashless Health insurance reduces paperwork related to reimbursement claims, simplifying the process by avoiding the submission of multiple documents and bills after treatment.

-

Access to Quality Care:

Cashless health insurance provides access to reputed hospitals, ensuring quality healthcare services.

-

Immediate Financial Relief:

Cashless health insurance offers immediate financial support, allowing patients and families to focus on treatment and recovery during medical emergencies.

-

Wide Network of Hospitals:

Leading insurance companies in India have a vast network of hospitals, ensuring the cashless facility can be accessed nationwide, including at multispecialty providers.

Types of Treatments Covered by Cashless Medical Insurance

A wide range of medical treatments is typically covered by cashless medical insurance. Common treatments include:

-

Hospitalization Costs:

Inpatient stay, nursing charges, doctor’s consultation fees, and surgery costs.

-

Pre- and Post-Hospitalization Expenses:

Medical expenses incurred before and after hospitalization, generally for a specified number of days.

-

Daycare Treatments:

Procedures not requiring 24-hour inpatient hospitalization, such as cataract surgery, dialysis, or chemotherapy.

-

Ambulance Charges:

Emergency transportation to the hospital via ambulance is often included in the policy.

-

Diagnostics and Medications:

Some policies cover diagnostic tests and prescribed medications during hospitalization.

Also Read: Things to consider while buying health insurance plans

Points to Consider When Opting for Cashless Medical Insurance

-

Network Hospitals:

Review the list of in-network hospitals before purchasing a policy to ensure that nearby, efficient, or preferred hospitals are part of the insurer’s network.

-

Claim Process Understanding:

Familiarity with the claim process is essential. Understand the time limits for notifying the insurance provider about planned or emergency hospitalization.

-

Coverage and Exclusions:

Read the policy carefully to understand what is covered. Some treatments or pre-existing conditions, like dental care, may be excluded.

-

Sub-Limits:

Some policies include sub-limits on treatments or hospital room types. For example, coverage may only extend to a shared room, and choosing a private room could result in additional costs.

-

Pre-Authorization:

Timely pre-authorization is crucial for a smooth cashless claim process. Completing this step can help avoid delays during hospitalization.

-

Partial Coverage:

Be mindful that not all expenses are covered under cashless insurance. For instance, toiletries, consumables, or registration fees may need to be paid out of pocket.

Conclusion

Selecting the right policy aligned with personal and family healthcare needs is an essential step in ensuring adequate coverage. A policy with a comprehensive network of hospitals, familiarity with the claim process, and awareness of sub-limits and exclusions is vital to maximizing the benefits of cashless medical insurance.

Are you interested in knowing what health insurance choices you have? For additional information, visit Elephant.in or give 1800 266 9693 a call or send an email to support@elephant.in!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/21

-

-

Published on: 16th Jan 2025Does Health Insurance Premium Increase with Age?READ MORE

Published on: 16th Jan 2025Does Health Insurance Premium Increase with Age?READ MOREIn order to protect yourself from the weight of medical expenses, getting health insurance is essential. Your health insurance premium changes as you grow older due to growing health risk concerns. To understand how age plays a key role in determining insurance premiums in India, we are going to take you through the relationship between age and insurance costs in this blog.

What are Health Insurance Premiums?

Payments that you make periodically to your particular insurance company for protection are called health insurance premiums. The type of coverage you choose, your lifestyle, age and state of health are certain factors upon which these premiums are calculated.

Determining Premiums: Age is a Key Factor

One of the main factors that affect health insurance premiums primarily is age. Your risk of a health issues arising increases as you grow older. When setting premium costs, insurance company take into consideration this increased risk. This is why age plays a key role:

-

Increased Risk of Health Issues:

-

Government Health Schemes:

Age related diseases like hypertension, heart problems and diabetes are more common in older individuals. It leads to higher claim costs for the insurance companies as treatments for these kind of diseases are costly.

Subsidized premiums are offered to senior citizens by some government health insurance schemes. However, certain limitations are implied on network hospitals and on coverage under these schemes.

Impact of Age on Premium Calculations

To calculate premiums based on various factors, including age, insurance companies utilize the actuarial models. Statistical probability of health insurance policy claims at different age groups are considered by these models. Your health insurance premiums may increase gradually to be in tune with the higher risk associated with the age group you are in as you age.

There are several other factors that influence your health insurance premium, leaving aside the most important factor that is age:

-

Health Status:

-

Lifestyle:

-

Sum Insured:

-

Network Hospitals:

You can be subjected higher premiums if there is a pre-existing medical condition or a family history of certain diseases.

Having a habit of smoking, consuming alcohol, or a sedentary lifestyle can lead to an increase in health risks and which in turn leads to an increase in premiums.

Having a high premium means that the sum insured is also high. An adequate sum insured should be chosen to make sure that the medical expenses are covered.

A greater flexibility in accessing healthcare is provided if an insurance plan with a wider network of hospitals is chosen but at the same time, the premiums for the same will be higher.

Steps to Manage Your Health Insurance Premium as You Age

- Lower premiums can be achieved for long term if you purchase health insurance at a young age.

- You can implement premium reduction tactics for health insurance by maintaining a healthy lifestyle, which can help lower your health risks.

- To make sure your health insurance policy is updated as per your health requirements, conduct frequent reviews.

- Subsidized premiums are offered to senior citizens under certain government health insurance schemes. Consider exploring those.

Conclusion

Despite being a significant factor, age is not the sole determinant of health insurance premiums. By understanding the various factors that impact your premium, you can make informed decisions when selecting a health insurance plan that provides adequate coverage at a reasonable price. Remember that prioritizing your health and leading a healthy lifestyle can help reduce the impact of aging on your insurance.

Are you curious about the benefits that health insurance could provide? To get more details, check out Elephant.in or contact 1800 266 9693 or email support@elephant.in!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/20

-

Published on: 27th Dec 2024Buying Health Insurance in Pune: Your Quick and Simple GuideREAD MORE

Published on: 27th Dec 2024Buying Health Insurance in Pune: Your Quick and Simple GuideREAD MOREThe vibrant city of Pune is famous for its lively culture and its ever growing healthcare facilities. In order to safeguard yourself and your family from unexpected hospitalization costs it is essential that you get yourself and your family a health insurance when living in Pune.

The process of acquiring health insurance, valuable information on various policies available, key factors to consider and the important steps to purchase will be highlighted in this blog post.

Understanding Health Insurance in Pune

To pay for various medical costs and hospitalisation costs, health insurance plans come into the play as a form of financial protection during such unexpected situations. Peace of mind can be achieved in situations where one is injured or sick due to the protection provided by the health insurance.

Benefits of Having Health Insurance in Pune

-

Financial Protection:

To avoid using up your savings and to pay for expensive medical expenses a health insurance is a must.

-

Access to Quality Healthcare:

Top notch hospitals and expert treatment can be utilised if one has a health insurance.

-

Cashless Hospitalization:

Cashless hospitalizations services can be availed which removes the necessity of making advance payments when one has health insurance.

-

Tax Benefits:

Through Section 80D of the Income Tax Act, the Indian government grants tax benefits for health insurance premiums

Types of Health Insurance Plans in Pune

In Pune, different kinds of health insurance policies can be found:

-

Individual Health Insurance:

Only an individual will be apt for this kind of coverage.

-

Family Floater Health Insurance:

All family members will be insured under this type of insurance coverage.

- For elderly individuals, this is specially created for elderly individuals./li>

-

Critical Illness Insurance:

In cases of serious illnesses, Critical Illness Insurance give a one-time payment to cover for the medical expenses.

Factors to Consider When Buying Health Insurance in Pune

-

Sum Insured:

To cover your medical costs considering your age, health factors and family size, select a proper sum insured.

-

Network Hospitals:

Choose a plan with an extensive hospital network in Pune for easy access to cashless medical care.

-

Pre-existing Conditions:

Make sure to verify coverage and waiting period for pre-existing conditions.

-

Add-on Covers:

Consider additional options such as maternity benefits, personal accident coverage, or dental insurance.

-

Premium Cost:

In order to choose the most favourable options, compare various insurance options and their rates.

-

Claim Settlement Ratio:

To comprehend an insurance company’s promptness, do a thorough investigation of their claim settlement ratio.

Also Read: A Step-By-Step Guide To Navigating Health Insurance Claims

Steps to Buy Health Insurance in Pune

-

Assess Your Needs:

Determine the required level of coverage by taking into account your age, health, and the size of your family.

-

Compare Plans:

Obtain quotations from many insurance companies, then compare the variations in features, costs, and coverage within the network.

-

Choose a Plan:

Select the solution that most closely matches your needs and budget.

-

Submit Documents:

Send in the proper paperwork, including proof of age, evidence of income, and (if needed) medical records.

-

Pay Premium:

Submit the first premium payment in order to initiate your policy.

Also Read: Factors Influencing Health Insurance Premiums: What You Need to Know

Tips for Managing Your Health Insurance

-

-

Renew Your Policy Timely:

To prevent gaps in coverage and ensure continuous benefits.

-

Update Your Insurer:

Notify your insurance provider of any updates to your address, health condition, or family information.

-

Read Your Policy:

Familiarize yourself with the policy’s terms and conditions to prevent confusion when making claims.

-

-

Maximize Benefits:

Utilize all the advantages provided by your health insurance coverage.

-

Utilize Online Services:

Numerous insurance companies provide online platforms for convenient management of policies and submission of claims.

Conclusion

Buying health insurance in Pune is necessary to protect your financial stability. Understanding the various kinds of plans, factors to think about, and steps included can help you make a knowledgeable choice and obtain a thorough policy that fits your exact requirements. Don’t forget, having a health insurance policy is a way to invest in your well-being and mental calmness.

Do you have interest in exploring the health insurance policies available to you? Get in touch with Elephant.in either by calling 1800 266 9693 or sending an email to support@elephant.in for more information, or simply visit Elephant.in!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/19

-

-

Published on: 27th Dec 2024How to Calculate Car Insurance Premium: A step-by-step guide to calculating your own car insurance premiumREAD MORE

Published on: 27th Dec 2024How to Calculate Car Insurance Premium: A step-by-step guide to calculating your own car insurance premiumREAD MOREFor every responsible car owner in India, acquiring car insurance is vital but it can be quite a task when it comes to determining the cost/premiums of the insurance. In order to help you make informed decisions and for you to accurately estimate your coverage costs, we will break down the important factors to consider in this insightful blog.

Getting familiar with Car Insurance

An individual is protected from unpredictable events such as accidents, theft/burglary or damage if he has car insurance policy. To ensure financial assistance in such scenarios, you pay a premium. The cost of your premiums may, however, be impacted by multiple variables.

-

Vehicle Type:

-

Distance Driven:

-

Location:

-

No Claim Bonus (NCB):

-

Coverage Options:

Opting for comprehensive car insurance coverage increases your expenses but protects your vehicle along with the mandatory Third Party Insurance.

-

Additional Features:

Key Influencers of Your Premium

Due to elevated costs of repairs for high-end luxury vehicles, they incur higher premium costs. Manageable premium rates are for economical cars such as hatchbacks.

Premiums can also be influenced by the amount of distance you have driven. Pay as you drive is a type of insurance the calculates the premium you will be paying as per the distance you have driven.

Your premium range can be affected as per the location your car is registered in. In densely populated or high-risk areas, your rates could rise, whereas they could decrease in less populated areas.

You might save around 50% on your own damage premiums by qualifying for NCB due to not making any claims in the previous year.

Adding extra coverage options such as zero depreciation cover and roadside assistance may result in higher premiums.

-

Select Your Coverage:

-

Determine Your IDV (Insured Declared Value):

-

Assess Add-On Options:

-

Review Your NCB:

-

Factor in Vehicle Details:

-

Provide Personal Information:

-

Use Online Calculators:

Steps to Estimate Your Premium

3rd-Party or Comprehensive Coverage is completely your choice

The current market value of your vehicle affects both the premium and compensation in the event of total loss.

Consider optional features and select only those essential to your coverage.

If you’ve maintained a claim-free record, you may be eligible for a reduced premium.

Age, make, and model of the vehicle impacts the overall premium.

Age, driving experience, and location also affect the final calculation.

Many online aggregators provide tools to help you calculate your premium based on the provided data.

Cost-Saving Strategies

- Choose a higher voluntary deductible to lower your insurance costs.

- Maintain a clean driving history to prevent costly penalties.

- The installation of anti-theft devices will enhance overall car safety and lower car insurance premiums.

Conclusion

Understanding all the factors that impact your insurance premiums makes it simple to make a well-informed choice and select a customized car insurance policy for yourself.

We are constantly available to assist you. Get in touch with us at 1800 266 9693 or send us an email at support@elephant.in for more information on car insurance options, or just head to Elephant.in!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/18

-

-

Published on: 11th Dec 2024What to Know About Insurance When Buying a New CarREAD MORE

Published on: 11th Dec 2024What to Know About Insurance When Buying a New CarREAD MOREEven though purchasing a new car can be a thrilling experience, it is important not to overlook one crucial aspect: car insurance. To protect your investment from any unpredictable situations, it is essential to know about the intricacies of car insurance. Here is a simple guide to assist in understanding car insurance while buying a new vehicle.

Get the Basics Right

Car insurance is an agreement between an individual and an insurance company that provides insurance coverage for vehicles. On receiving the premium amount, the insurance company will cover specific expenses in case of damage, theft, or accidents involving your car.

In India, it is required by law to have third-party car insurance. It includes payments for harm or injuries to others, excluding damage to your personal vehicle. Choosing full coverage insurance is advised because it includes protection for both third-party losses and any damages to your own car.

Types of Car Insurance

-

Comprehensive Insurance:

-

3rd Party Insurance:

Both third-party claims and damages to your vehicle are covered. While more expensive, the extensive protection offered can provide peace of mind.

As the minimum required by law, this covers damages to others but leaves your vehicle unprotected. Although cheaper, this option could expose you to additional costs if the vehicle sustains damage.

What Influences Your Premium?

-

Car Make and Model:

-

Age of the Car:

-

Location:

-

Driving History:

-

Coverage Type:

Extensive protection is provided when one acquires a comprehensive car insurance, even though it costs more.

Higher premiums are typically attracted by high-end vehicles due to increased repair costs.

Older cars generally come with lower premiums because of reduced market value.

Living in metropolitan areas can lead to higher premiums due to greater risks of accidents or theft.

Lower premiums can be earned by maintaining a clean driving record, as it suggests a lower risk to insurers.

Also Read: Understanding Different Types of Car Insurance Coverage

The No Claim Bonus (NCB)

The No Claim Bonus (NCB) serves as an incentive for drivers who exhibit responsible behavior on the road. If there are no claims filed within the policy year, policyholders can receive a discount of up to 50% on their own damage premium for the next year. This helps to save money and promote safer driving behaviors.

Understanding Insured Declared Value (IDV)

The maximum amount that the insurance company will pay out in the event that the vehicle is declared stolen, or a total loss is the IDV, which represents the car’s present value. Better coverage is provided by a higher insured stated value; nevertheless, the premium is usually higher. It is critical to strike the ideal balance between scope and expense.

Exploring Add-ons and Riders

-

Zero Depreciation Cover:

-

Engine Protection:

-

Roadside Assistance:

Provides peace of mind if the vehicle breaks down.

Full compensation is provided without accounting for depreciation, making this a smart choice for new car owners.

Covers engine damage from specific issues like waterlogging—a real concern in some areas.

Choosing the Right Insurance

-

Compare Policies:

-

Assess Premium vs. Coverage:

-

Check Claim Settlement Ratios:

-

Read the Fine Print:

-

Consider Your Driving Patterns:

You will come across a good car insurance policy after scouting through different plans and their quotes both online and offline.

Ensure the policy meets protection needs, rather than simply opting for the cheapest option.

This indicates how effectively an insurer handles claims—an essential factor in the decision.

Comprehend what is covered and not covered to prevent unexpected surprises in the future.

Regular drivers or individuals in high-risk locations could see greater advantages with comprehensive insurance.

Insuring Your New Car

Though dealers commonly provide insurance at the time of sale, it may not always be the most advantageous option. Make sure to compare quotes from different providers as many of them have fast online quotes available for a more efficient evaluation of options.

Don’t Forget Your NCB Transfer

When upgrading from an old car, transferring the No Claim Bonus to the new policy can lead to significant savings. Insurers should be notified about the NCB transfer during the purchase process.

Navigating the Claims Process

- Insurers should be notified immediately after an incident.

- A police report should be filed if needed, especially for theft or major accidents.

- A claim form should be submitted to the insurance company.

- Necessary documents, such as a driving license and car registration, must be provided.

- The insurer should inspect the car to assess the damage.

Conclusion

Getting the proper insurance for a new car is just as important as buying the car itself. By understanding the fundamentals, conducting comparisons, and making knowledgeable choices, both vehicle and financial protection can be guaranteed. Always aim for a balance between coverage and cost to find the ideal policy.

Reach out at 1800 266 9693, email support@elephant.in, or visit Elephant.in to explore car insurance options!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/18 -

-

Published on: 25th Sep 2024Buying Health Insurance in Delhi Made Easy: Here’s HowREAD MORE

Published on: 25th Sep 2024Buying Health Insurance in Delhi Made Easy: Here’s HowREAD MOREThe bustling metropolis of Delhi also has serious health issues. Due to rising medical care costs and pollution, many view health care coverage as imperative. We will help you in understanding the steps and things to look out for while purchasing health insurance in Delhi through our blog post.

Are You Buying Health Insurance? Consider These Factors:

-

Sum Insured:

This shows the maximum amount your insurance company will pay for medical bills over a full year. A bigger insured sum is associated with more comprehensive coverage.

-

Coverage:

Analyze the insurance details thoroughly. While many plans cover hospital stays, surgeries, and prescription meds, others may also cover dental care, maternity care, and coverage for severe illnesses.

-

Network Hospitals:

Your insurance company is connected to these medical facilities. Selecting a provider from the network helps streamline the claims process and perhaps save expenses.

-

Waiting Period:

Some claims, such as those involving pre-existing conditions, can be filed within this time frame.

-

Premium:

This is the sum you pay the insurance supplier to keep up with the contract’s status. Comparing the premiums offered by various suppliers is essential.

Also Read: A Step-By-Step Guide To Navigating Health Insurance Claims

Choosing the Right Plan

Health insurance plans come in various forms. Common types include:

- Individual Health Insurance: Tailored for single individuals.

- Family Floater Plan: Covers you, your partner, and your dependent children under a single insurance.

- Senior Citizen Health Insurance: Health insurance specifically created for older individuals.

Numerous factors, including age, the number of family members, existing medical conditions, and financial status, influence which plan is ideal.

Things to Look Out for When Purchasing Health Insurance

-

Comprehensive Comparison:

Evaluate the premiums, hospital network, and claim settlement rates of various insurance companies along with their coverage.

-

Meticulous Policy Review:

Thoroughly understand the policy terms and conditions before purchase.

-

Reputable Insurer Selection:

Prioritize insurers with a proven track record of claim settlements.

-

Exploring Add-on Covers:

Consider supplementary covers like critical illness, personal accident, or maternity for enhanced protection.

-

Regular Policy Assessment:

As life evolves, so do insurance needs. Periodically review your policy to ensure it aligns with your changing requirements.

The Claim Process

Quickly informing your insurance provider is essential if there is a medical emergency. A few guarantors give the choice of hospitalization without cash at clinics inside their organization. In cases without a credit only office, you might need to pay for costs forthright and afterward look for repayment from the insurance agency.

Also Read: 10 Sneaky Reasons Your Health Insurance Claim May Not Get Approved

Conclusion

Despite the fact that purchasing health insurance can be overwhelming, it is necessary for financial readiness. By completely surveying your needs, assessing various choices, and picking a dependable insurance agency, you can establish a strong health insurance foundation for yourself as well as your friends and family.

Please feel free to call us at 1800 266 9693 or email support@elephant.in with any questions. For excellent choices for vehicle insurance, visit Elephant.in!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/16

-

-

Published on: 05th Sep 2024How to Protect Your Home Loan with Term Insurance?READ MORE

Published on: 05th Sep 2024How to Protect Your Home Loan with Term Insurance?READ MOREHome is a dream which everyone sees with equivalent enthusiasm. And why not? It is a symbol of stability and testament to hard work that one does. However, no doubt it demands substantial financial commitment that has to be promised in terms of monetary supply. Seemingly, while owning a home is a rewarding experience, it’s equally important to protect this investment for your family. But how? Well, this is where term insurance steps in as a crucial financial safety net.

Importance of Term Insurance

The insurance policy, designed to provide financial protection for a limited period of time, is generally called term insurance. Term insurance is not like ordinary life insurance, giving maturity benefits; it rather pays in bulk in case the policyholder unfortunately dies anytime during the policy term.

Also Read: How much term insurance cover do I need?

Why Term Insurance is Important for Homeowners

A term life cover helps protect the house you’ve built for your family through your hard work and effort, especially if something unfortunate happens and the main earner passes away. With term insurance, your loved ones can use the insurance money to pay off the remaining home loan. This ensures they can continue living in the same house without the burden of a significant debt.

Knowing your family will be okay money-wise even if you’re not around gives you peace of mind. Many people find this hard to achieve. If something unexpected happens, it helps your family with much-needed money.

In today’s busy world where inflation keeps hiking up, term insurance is a cheaper insurance plan to buy. This makes it a good choice for people who have financial responsibilities like home loans and want to protect what they own.

How Much Term Insurance Coverage Do You Need?

Figuring out the right amount of term insurance coverage is key. Here’s a basic guide:

-

A Backup for Home Loan Repayment

-

Extra Coverage:

-

Check Often:

Term insurance can also serve as a safeguard in case of any unforeseen circumstances affecting the home loan repayment. It offers an option to settle outstanding debts including home loan, provided the insured sum equals or exceeds the outstanding loan amount.

Think about adding a safety net to the insured sum to handle other money matters like daily costs, kids’ schooling, or other debts.

As your loan shrinks and money responsibilities shift, look over your term insurance coverage to make sure it fits your current needs.

Also Read:Factors to consider while buying Term Life Insurance

Picking the Best Term Insurance Plan

Choosing the Best Term Insurance plan requires considering a few factors:

-

Policy

-

Sum Insured

-

Additional Policy Features

-

Leverage Your Policy for Loans:

-

Cost

The policy should at least be concurrent with the home loan, or a little beyond that to provide additional coverage.

Your outstanding house loan and other debt liabilities should be the basis for arriving at the sum insured.

Few policies will let you add extras, like serious illness cover or benefits in the event of death or disablement due to an accident. Consider whether you need these, based on your needs and your ability to pay for them.

Term insurance policy can be used as a collateral for a loan, allowing lender to claim the policy benefit in case of default.

Prices from different insurance companies should be compared to get value for the money.

Conclusion

This might seem like an expenditure additional to the one paid for buying insurance, but actually, it is an investment for your family’s future. The sense of security that one has by being prepared for the contingency offsets the initial cost incurred.

Want to know your options? Call now at 1800 266 9693 or mail at support@elephant.in. Want to know more about how to protect your vehicle? Log on to Elephant.in to know more about our extensive car insurance plans!

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/15

-

-

Published on: 30th Aug 2024Factors Influencing Health Insurance Premiums: What You Need to KnowREAD MORE

Published on: 30th Aug 2024Factors Influencing Health Insurance Premiums: What You Need to KnowREAD MOREHealth care expenses are spiraling day by day. In modern India, a health insurance plan has indeed become more of a need than a luxury. Not to forget that it actually is a financial shield, saving you from the burden of medical bills due to any mishap, for example, hospitalization or falling ill. But as new and established insurance companies alike pitch all manner of health insurance plans, at least one question seems to keep arising: Which is best, and how much is it going to cost me?

It doesn’t matter; we are there to help you. Various factors have a bearing on health insurance premiums in India, thus providing you with three sources to make an empowered decision while choosing a health insurance plan. You will be able to compare plans with purpose and choose the best health insurance policy that works well for you and your pocket.

Health Insurance Premiums

A health insurance premium may simply be put in the same league with the price a person is to pay in regards to a linsurance company on a monthly or annual basis in order to receive coverage. Such coverage assures one of compensation up to a pre-determined limit whenever the individual falls ill or needs admission into a hospital for due reasons. Your premium is likely, in most cases, to dictate just how comprehensive your cover turns out to be.

Factors Affecting Your Health Insurance Premium

The health insurance premium depends upon a various factors. Let us discuss some of the most important ones:

-

Age:

In general, premium rates for health insurance are charged on a lower rate for the younger age group in comparison to older people. This is because, with an increase in age, the risk for hospitalization and the associated medical cost increases.

-

Your Health Status:

If you enjoy the best premiums; then your pre-existing conditions, if any, may lead you into hefty premiums, as the company estimates probability.

-

Your Lifestyle:

Such habits as smoking or using tobacco will raise your premiums in a huge way. This is because such activities are dangerous to your health status.

-

Sum Insured:

This is the maximum amount that an insurance company is inclined to pay toward any treatment expenses. Quite normally, the higher the sum insured, the higher the premium, which in turn should ensure adequate coverage.

-

Your Policy Coverage:

The premium will be less for a basic policy with restricted coverage as compared to comprehensive policies covering a wide scope of benefits, including pre- and post-hospitalization expenses or critical illness cover.

-

Your Location:

Geographical location may have an impact on your medical costs; it differs by city or region. So in case you reside in a metro city with higher healthcare costs, your premium may turn out a bit on the higher side.

-

Claim History:

A history of regular claims often makes insurance companies take it as an indicator to place you at an above-average risk, for which they might go ahead and increase the premium upon renewal.

Cost vs. Coverage: The Trade-Off

The more competitive premium may be inviting, but here is a trade-off between cost and cover: one with a low enough premium in a basic plan will not give any significant coverage against serious medical conditions that might demand high-cost treatment.

Tips for Managing Your Health Insurance Premium

Here are some extra pointers to keep your health insurance premium in check:

- Assess your medical requirements and select a plan that provides sufficient coverage without superfluous features

- Maintaining excellent habits and living a healthy lifestyle will help you save money on premiums over time

- Never accept the first plan you come upon. To compare costs and coverage choices, get quotations from many insurance providers

- A family floater plan might be an affordable choice if you have a family because it covers several individuals under a same policy

- If you didn’t file any claims the year before, many insurance companies may give you a No Claim Bonus on your Health Insurance renewal premiums

Conclusion

Once you understand what creates variations in your health insurance premiums, you will be better equipped to make informed decisions while choosing a plan. Keep in mind that the best health insurance plan is not about the affordability but the proper balance between cost and comprehensive coverage based on the needs of the buyer. There are so many ways to be smart about your health; one of these is to choose a health insurance plan that’s got your back—and your family’s—in case any medically unexpected situation arises.

*Terms and conditions apply. The information provided in this article is generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. You are recommended to obtain specific professional advice from before you take any/refrain from any action. Tax benefits are subject to changes in tax laws. Please contact your tax consultant for an exact calculation of your tax liabilities.| EL/BLOGS/24-25/14

-

Our Insurance Partners

What our Customers Say

-

For HRAs part of our employee benefits initiative, we recently implemented Elephant.in for our corporate employees, and we are very satisfied with the service. With enticing discounts, employees were able to choose from a pool of well-curated insurance products. You're doing a great job, Elephant.in

Anant NagvekarCompliance Officer - Brunel India Pvt Ltd

Anant NagvekarCompliance Officer - Brunel India Pvt Ltd -

For HRElephant.in was recently onboarded into our organisation and the integration process went very smoothly. Our employees were given exclusive deals on well-curated insurance products to choose from. Congratulations, Elephant.in!

Shubha ShettyHR Manager -Marathon Realty

Shubha ShettyHR Manager -Marathon Realty -

For HRMy car insurance policy was purchased from Elephant.in, and I am really pleased with my overall experience. Their AI-based recommendation, as well as multiple options from other insurance companies, were presented to me, resulting in a fantastic range of options to choose from, all at exceptional discounts when I used my work email ID. Cheers to Team Elephant.in!

Aashish MajumdarFinance Head - INOX Air Products Pvt. Ltd.

Aashish MajumdarFinance Head - INOX Air Products Pvt. Ltd. -

For HrWe recently rolled out Elephant. in as a voluntary insurance program for our employees’ personal insurance requirements. Being a cost-free employee benefit initiative, our employees now have access to their insurance products at exclusive discounts and offers. Thank you, Team Elephant.in!

Anil DhaleHead-HR -INOX Air Products Pvt. Ltd.

Anil DhaleHead-HR -INOX Air Products Pvt. Ltd. -

For CustomersI have got a reference of Elephant Insurance for purchasing term life insurance through the organisation that I work with. Website is designed to recommend the right policy without confusing with loads of options. There after insurance advisor does a very professional job of clarifying and suggesting the right policies, filling in required forms and following up with the insurance company till the policy is successfully assigned. Great experience with Elephant and their team. Ajay Pitale, my insurance advisor was knowledgeable, professional and extremely patient. He allowed me space to decide and also followed up when there were issues in counter offers till they are closed. He was prompt in his responses. Sonali Borkar from the operations team was very prompt in escalating to the insurance and get the required resolution. I'm impressed with the knowledge, availability of Elephant team and prompt resolution of queries.

Venkat ReddyDelivery Head-Wipro

Venkat ReddyDelivery Head-Wipro -

For customersI have purchased Car insurance and got a flat 80% off on my purchase. Their customer service team ensured all my queries with regards to my policy were resolved quickly. Thank you , team Elephant for this wonderful experience, you are highly recommended to all my friends and colleagues.

Dilip ChorgeManager Treasury Operations - Cotmac Electronics Private Limited

Dilip ChorgeManager Treasury Operations - Cotmac Electronics Private Limited -

For customersExtremely happy with the services of Elephant.in. The Customer Support staff is very supportive. Mr. Vivek Vishwakarma helped us in the understanding critical procedure of claims and guided us on each step for hassle-free claim approval.

Avinash AgrawalTeam Leader - Sanjeev Auto Parts Manufactures Pvt Ltd

-

For customersMr.Vinayak Jadhav – Mumbai office & Mrs Chitra Nagarajan – Chennai office are very excellent support and helpful for policy renewal and policy claims on time.

Magesh .VAdmin- SPR constructions

Magesh .VAdmin- SPR constructions -

For customersI topped up my Health Insurance policy with a Super Top-up, both products were purchased from Elephant.in. I appreciate the excellent discounts and the advice from my relationship manager, who helped me gain attractive add-on benefits. Great service Team Elephant.in, Keep it up!

Akhilendra SinghWelspun Enterprises Limited

-

For customersElephant.in is definitely my go-to insurance website after I purchased car insurance for my new car from them. Right from giving me prompt quotations to getting the lowest possible rate in the market, they helped me all throughout. I had done thorough research on all offline and online channels, but their corporate deal was the best. Special shoutout to Nikita from their customer service team who was just one call away for all my queries. Great going guys!

Udit JainAssitant Vice President-ANAROCK Retail

Udit JainAssitant Vice President-ANAROCK Retail -

For customersI bought a Car insurance from Elephant.in and got an amazing discount of flat 80% that helped me to save a lot of money! Elephant.in . Great service team!

Diwakar MishraScrum Lead- Optum

Diwakar MishraScrum Lead- Optum -

For customersAs compared to Health Insurance plans available online, Elephant.in gave me exclusive features at unbeatable price which I could happily share with my entire group of friends !

Kanika MathurFounder-Ink Dream

Kanika MathurFounder-Ink Dream -

For customersThe Senior Citizen insurance covers from Elephant.in was the ideal gift I got for my parents for their anniversary. The recommendation feature on the website was a huge help at a price point was quite affordable for a younger professional like me.

Yash PandyaTech Cordinator-A- Media INC

-

For customersI highly recommend Elephant.in . I had purchased a Super Top Up policy and the top-up available at Elephant.in had many features as compared to the products available in the market. I am happy with the product and price offered.

Prateek MundharaCharacter Animator-Redefine

-

For customersI just renewed my car insurance + home insurance. The renewal process was pretty smooth and the UI was good

Sachin KaulgudSr. Vice President -Alliance Insurance Brokers

-

For customersThank you team Elephant for all your help and support in making this seamless and smooth for me. I appreciate your constant support.

Shyamala ShuklaGroup VP, Talent Acquistion, Corporate Human Resources- CK Birla Group

Shyamala ShuklaGroup VP, Talent Acquistion, Corporate Human Resources- CK Birla Group -

For customersI was happy to have team Elephant.in's support for my policy processing. All my documentation and clearance process were completed smoothly with your support. It was a nice experience interacting with you and I hope you continue the same for other customers as well who really need such guidance. I wish you and your organization all the best

Vikas KumarLead Technical Consultant -Mando Softtech India Private Limited

-

For customersPurchasing health insurance from Elephant.in was a win-win situation for me, it helped me protect my health and save money on taxes- all of this through a web portal that was extremely easy to navigate.

Sherene AftabFounder- Serene Hour Counselling & Career Advice Consultancy

Sherene AftabFounder- Serene Hour Counselling & Career Advice Consultancy -

For customersExcellent support and customer service from team Elephant.in. Their website is easy to navigate, and the price are truly discounted. Overall great experience !

Chintan KapadiaHigh Ground Enterprise Limited -Director

Chintan KapadiaHigh Ground Enterprise Limited -Director -

For customersTeam elephant has been extremely cooperative and helpful, their customer service is truly commendable

Sharom B MubarakaiOwner -Horticulturist

Sharom B MubarakaiOwner -Horticulturist -

For customersI am delighted to share my experience with Elephant team, Especially Sonali & Subhan who has always been on toes for help & resolving queries at the earliest possible, your customer-centricity & efforts are highly valued, Many thanks for getting the policy issued in such a small period of time, looking for similar efforts in future as well.

Ashish JainFinance Assistant Manager -Pidilite Industries

-

For customersTeam Elephant.in ensured amazing features and exclusive discounts on my health insurance renewal using my work email ID. I am extremely happy with their consistent service year on year.

Sameer WalgudeSourcing Business Partnering- Mahindra & Mahindra Limited, AFS (Auto & Farm Equipment Sectors)

-

For customersIt was extremely easy to purchase the Term Life insurance on the elephant.in Portal. The Journey was user Friendly and could be completed with just few clicks. Moreover, the support I received during Policy issuance was well appreciated

Nikhil HemrajaniCo-Founder-Sitara Studios

Nikhil HemrajaniCo-Founder-Sitara Studios -

For customersTopping up my existing health plan with an affordable Super top-up from elephant.in was a huge relief, given the pandemic and multiple rising medical expenses that come along with it.

Smita ChavanFounder -Sk Food & Hosptality

Smita ChavanFounder -Sk Food & Hosptality -

For customersTeam Elephant was extremely professional, they helped me understand the idea of insurance and the importance of term insurance, they also shared all the best options available for me and resolved all my queries. I have a wonderful experience and will recommend Elephant.in to our friends

Brijesh Kumar SinghLead Software Engineer -Informatica

Brijesh Kumar SinghLead Software Engineer -Informatica -

For customersA great discount of 80% on my car insurance policy! Elephant definitely delivers what they promise!

Saurabh ManchandaManager- Victora Hospitalities

-

For customersI fully recommend elephant.in. I received a killer discount on my car insurance policy and the process was quick and easy

Avdesh ChauhanSupplier Quality Manager-Andritz Hydro

-

For CustomersI have purchased Car insurance and got a flat 80% off on my purchase. Their customer service team ensured all my queries with regards to my policy were resolved quickly. Thank you , team Elephant for this wonderful experience, you are highly recommended to all my friends and colleagues.

Dilip ChorgeManager Treasury Operations - Cotmac Electronics Private Limited

-

For CustomersExtremely happy with the services of Elephant.in. The Customer Support staff is very supportive. Mr. Vivek Vishwakarma helped us in the understanding critical procedure of claims and guided us on each step for hassle-free claim approval.

Avinash AgrawalTeam Leader - Sanjeev Auto Parts Manufactures Pvt Ltd

-

For CustomersMr.Vinayak Jadhav – Mumbai office & Mrs Chitra Nagarajan – Chennai office are very excellent support and helpful for policy renewal and policy claims on time.

Magesh .VAdmin- SPR constructions

-

For CustomersI topped up my Health Insurance policy with a Super Top-up, both products were purchased from Elephant.in. I appreciate the excellent discounts and the advice from my relationship manager, who helped me gain attractive add-on benefits. Great service Team Elephant.in, Keep it up!

Akhilendra SinghWelspun Enterprises Limited

-

For CustomersElephant.in is definitely my go-to insurance website after I purchased car insurance for my new car from them. Right from giving me prompt quotations to getting the lowest possible rate in the market, they helped me all throughout. I had done thorough research on all offline and online channels, but their corporate deal was the best. Special shoutout to Nikita from their customer service team who was just one call away for all my queries. Great going guys!

Udit JainAssitant Vice President-ANAROCK Retail

-

For CustomersI bought a Car insurance from Elephant.in and got an amazing discount of flat 80% that helped me to save a lot of money! Elephant.in . Great service team!

Diwakar MishraScrum Lead- Optum

-

For CustomersAs compared to Health Insurance plans available online, Elephant.in gave me exclusive features at unbeatable price which I could happily share with my entire group of friends !

Kanika MathurFounder-Ink Dream

-

For CustomersThe Senior Citizen insurance covers from Elephant.in was the ideal gift I got for my parents for their anniversary. The recommendation feature on the website was a huge help at a price point was quite affordable for a younger professional like me.

Yash PandyaTech Cordinator-A- Media INC

-

For CustomersI highly recommend Elephant.in . I had purchased a Super Top Up policy and the top-up available at Elephant.in had many features as compared to the products available in the market. I am happy with the product and price offered.

Prateek MundharaCharacter Animator-Redefine

-

For CustomersI just renewed my car insurance + home insurance. The renewal process was pretty smooth and the UI was good

Sachin KaulgudSr. Vice President -Alliance Insurance Brokers

-

For CustomersThank you team Elephant for all your help and support in making this seamless and smooth for me. I appreciate your constant support.

Shyamala ShuklaGroup VP, Talent Acquistion, Corporate Human Resources- CK Birla Group

-

For CustomersI was happy to have team Elephant.in's support for my policy processing. All my documentation and clearance process were completed smoothly with your support. It was a nice experience interacting with you and I hope you continue the same for other customers as well who really need such guidance. I wish you and your organization all the best

Vikas KumarLead Technical Consultant -Mando Softtech India Private Limited

-

For CustomersPurchasing health insurance from Elephant.in was a win-win situation for me, it helped me protect my health and save money on taxes- all of this through a web portal that was extremely easy to navigate.

Sherene AftabFounder- Serene Hour Counselling & Career Advice Consultancy

-

For CustomersExcellent support and customer service from team Elephant.in. Their website is easy to navigate, and the price are truly discounted. Overall great experience !

Chintan KapadiaHigh Ground Enterprise Limited -Director

-

For CustomersTeam elephant has been extremely cooperative and helpful, their customer service is truly commendable

Sharom B MubarakaiOwner -Horticulturist

-

For CustomersI am delighted to share my experience with Elephant team, Especially Sonali & Subhan who has always been on toes for help & resolving queries at the earliest possible, your customer-centricity & efforts are highly valued, Many thanks for getting the policy issued in such a small period of time, looking for similar efforts in future as well.

Ashish JainFinance Assistant Manager -Pidilite Industries

-

For CustomersTeam Elephant.in ensured amazing features and exclusive discounts on my health insurance renewal using my work email ID. I am extremely happy with their consistent service year on year.

Sameer WalgudeSourcing Business Partnering- Mahindra & Mahindra Limited, AFS (Auto & Farm Equipment Sectors)

-

For CustomersIt was extremely easy to purchase the Term Life insurance on the elephant.in Portal. The Journey was user Friendly and could be completed with just few clicks. Moreover, the support I received during Policy issuance was well appreciated

Nikhil HemrajaniCo-Founder-Sitara Studios

-

For CustomersTopping up my existing health plan with an affordable Super top-up from elephant.in was a huge relief, given the pandemic and multiple rising medical expenses that come along with it.

Smita ChavanFounder -Sk Food & Hosptality

-

For CustomersTeam Elephant was extremely professional, they helped me understand the idea of insurance and the importance of term insurance, they also shared all the best options available for me and resolved all my queries. I have a wonderful experience and will recommend Elephant.in to our friends

Brijesh Kumar SinghLead Software Engineer -Informatica

-

For CustomersA great discount of 80% on my car insurance policy! Elephant definitely delivers what they promise!

Saurabh ManchandaManager- Victora Hospitalities

-

For CustomersI fully recommend elephant.in. I received a killer discount on my car insurance policy and the process was quick and easy

Avdesh ChauhanSupplier Quality Manager-Andritz Hydro

-

For CustomersI have good support from your team and I am very very happy with your services

Vijay PillaiDeputy Manager -Jash Engineers

Vijay PillaiDeputy Manager -Jash Engineers -

For CustomersI wholeheartedly recommend elephant.in for any insurance policies that you require. They offered killer discounts, and the Ai recommendations provided solution based on my requirements.

Lithin KotianSpecialist Engineer -Mando Softech

-

For CustomersI purchased health insurance for my parents from Elephant.in, their senior citizen-friendly features and affordable pricing make it a must-buy for your loved ones

Dr. Abhishek SinghMDS - Periodontology and Implantology - Owner of "House of Smile"

Dr. Abhishek SinghMDS - Periodontology and Implantology - Owner of "House of Smile" -

For CustomersElephant.in delivered what they promised, a flat 80% discount on Car Insurance with amazing customer service. What more could a customer want !

Jayesh VaruFounder-Plain Canvas

Jayesh VaruFounder-Plain Canvas -

For CustomersI recently purchased Term Life insurance from elephant.in and the process was seamless. The Relationship Manager also made recommendations keeping tax planning in mind, which was extremely beneficial.

Salomi PujaraCreative Designer and Founder- All Smile Media Solutions

Salomi PujaraCreative Designer and Founder- All Smile Media Solutions -

For CustomersLimited Pay was a very helpful option while purchasing Term Life insurance and I am thankful to team Elephant.in for recommending it.

Ameya BhusariLead Engineer-KTM

Ameya BhusariLead Engineer-KTM -

For CustomersI topped up my existing health cover with Supertop-up from Elephant.in and I have been quite happy with the coverages, price point and support shared by their team

M . VirupakshaiahRegional Sales Manager -RPSG - Apricot Foods Pvt Ltd

-

For CustomersThe health policy I purchased for my parents from Elephant.in was cheaper as compared to the market and out of the many features they provided the best one was 'no medical test' before issuing the policy.

Namrata GonbareMH Jain & Company Associates -Accountant

Namrata GonbareMH Jain & Company Associates -Accountant -

For CustomersI came across the concept of a Super Top Up policy during the webinar conducted by Elephant.in. The features they shared and price point at which I purchased the product was excellent

Ankit KumarManager- Fyntune

Ankit KumarManager- Fyntune -

For CustomersI purchased Term Life insurance from elephant.in and their AI based recommendations followed by a very supportive customer service team made the whole process seamless

Pushkar YadavDirector-Corner Pixel Studios

Pushkar YadavDirector-Corner Pixel Studios -

For CustomersDear Team Elephant, I have received my refund really appreciate your kind support and cooperation over the hassle-free purchases. I would definitely recommend elephant to others as well.

Vishal BajpaiProject Manager-Andritz Hydro

Vishal BajpaiProject Manager-Andritz Hydro -

For CustomersI fully recommend Elephant.in. I received a huge discount on my car insurance policy and the process was quick and easy

Venkatesh SrinivasanLead Technical Support Engineer -Informatica

-